The

Australian Taxation Office (ATO) is one of the most sophisticated tax authorities in the world when it comes to cryptocurrency enforcement. It runs an active data-matching program covering every major Australian and international exchange, has sent warning letters to more than 350,000 Australian crypto holders, and treats virtually every crypto transaction — from straightforward sales toDeFi

yield farming — as a potential taxable event.

Yet many Australian investors still operate without a clear understanding of their obligations. The result is avoidable tax bills, compliance exposure, and missed opportunities to legally reduce what they owe.

This guide is designed to close that gap. Whether you are a long-term Bitcoin holder, an

SMSF trustee exploring digital asset allocation

, or an active trader navigating DeFi and NFTs, what follows is a comprehensive, plain-English breakdown of how crypto is taxed in Australia — and what smart investors do to stay ahead of it.

The foundational principle underpinning all Australian crypto taxation is straightforward: the

ATO classifies cryptocurrency as property

— specifically, as a

Capital Gains Tax (CGT)

asset — not as money or foreign currency.

This classification, which applies to Bitcoin, Ethereum, altcoins, stablecoins, NFTs, and tokens of every kind, has profound implications. It means that almost every time you transact with crypto — selling it, swapping it, spending it, gifting it — you are triggering a potential tax event. The same rules that apply when you sell shares or investment property apply when you dispose of digital assets.

Depending on the nature of your activity, the ATO may also classify crypto receipts as ordinary income rather than capital gains. The distinction matters enormously, because income is taxed at your full marginal rate, while capital gains attract a 50% discount for assets held longer than 12 months.

Core principle:

The ATO does not care which exchange you used, whether the exchange is Australian or offshore, or whether you converted to AUD before year-end. If you are an Australian tax resident, you are taxed on worldwide crypto income and gains. Every transaction must be recorded in AUD.

The ATO distinguishes between two types of crypto participants, and the tax treatment differs significantly between them:

Investor:

Holds crypto as a capital asset with a long-term view. Gains and losses are subject to CGT rules, and the 50% CGT discount applies to assets held for more than 12 months. This is the most common classification for private individuals.

Trader:

Carries on a business of buying and selling crypto to generate income. Gains are treated as ordinary business income (not capital gains), the 50% CGT discount does not apply, but legitimate business expenses are deductible. The ATO looks at factors including transaction frequency, volume, profit intent, and the degree of organisation and sophistication of the activity.

The line between investor and trader is not always clear, and the ATO makes this determination based on the totality of your circumstances. If you are unsure which category applies to you, consider reaching out to

NAX Capital's team

or a tax professional experienced in digital assets.

One of the most common misconceptions among Australian crypto holders is that tax only applies when you convert crypto to Australian dollars. This is incorrect. The ATO defines a taxable disposal broadly — any change in

beneficial ownership

of a crypto asset is a potential CGT event.

Selling crypto for AUD or another fiat currency

Swapping one cryptocurrency for another (e.g., trading Bitcoin for Ethereum — this is a disposal of Bitcoin at its market value)

Spending crypto on goods or services (unless the personal use asset exemption applies — see Section 5)

Gifting crypto to another person (treated as a disposal at the asset's market value on the date of the gift)

Receiving new tokens in a chain split or hard fork (where you did not hold the originating asset — typically a cost base of zero applies)

Depositing into certain DeFi protocols (where beneficial ownership is transferred to the protocol)

Staking rewards and yield (declared as income at the AUD market value on the date of receipt)

Mining rewards (income at market value when received, unless hobby-level activity)

Airdrops

(most are ordinary income at receipt value; initial allocation airdrops may be exempt — check ATO guidance)

DeFi interest and lending yield (income in the year earned, at market value when received)

Referral bonuses and sign-up rewards (included in assessable income at fair market value)

Salary or wages paid in crypto (taxed as income at the AUD value on the date of receipt)

Buying crypto with AUD (acquisition, not disposal — no tax event at purchase)

Transferring between your own wallets (no change in beneficial ownership — not taxable, but you must maintain records proving both wallets are yours)

Inheriting crypto (no CGT triggered on inheritance; the recipient's cost base is the market value at the date of inheritance)

Losses from theft or negligence (may be claimable as a capital loss, but the ATO requires strong documentary evidence that the asset is permanently inaccessible)

ATO Warning:

The ATO's data-matching program collects transaction data from exchanges including Binance, Coinbase, CoinSpot, and international platforms. Failing to declare crypto income or gains is not a grey area — it is a compliance breach that attracts penalties and interest.

For most Australian investors, the calculation follows a straightforward formula: the proceeds from the disposal (in AUD) minus the

cost base

of the asset equals your capital gain or loss.

The purchase price in AUD at the time of acquisition

Any brokerage fees or exchange transaction fees paid at acquisition

Any fees paid at disposal (these reduce your proceeds)

For crypto received as income (staking rewards, airdrops, etc.), the cost base is the AUD market value at the time of receipt — which is the same figure you declared as income. This is why working with a

licensed brokerage like NAX Capital

that provides audit-ready transaction records matters so much at tax time.

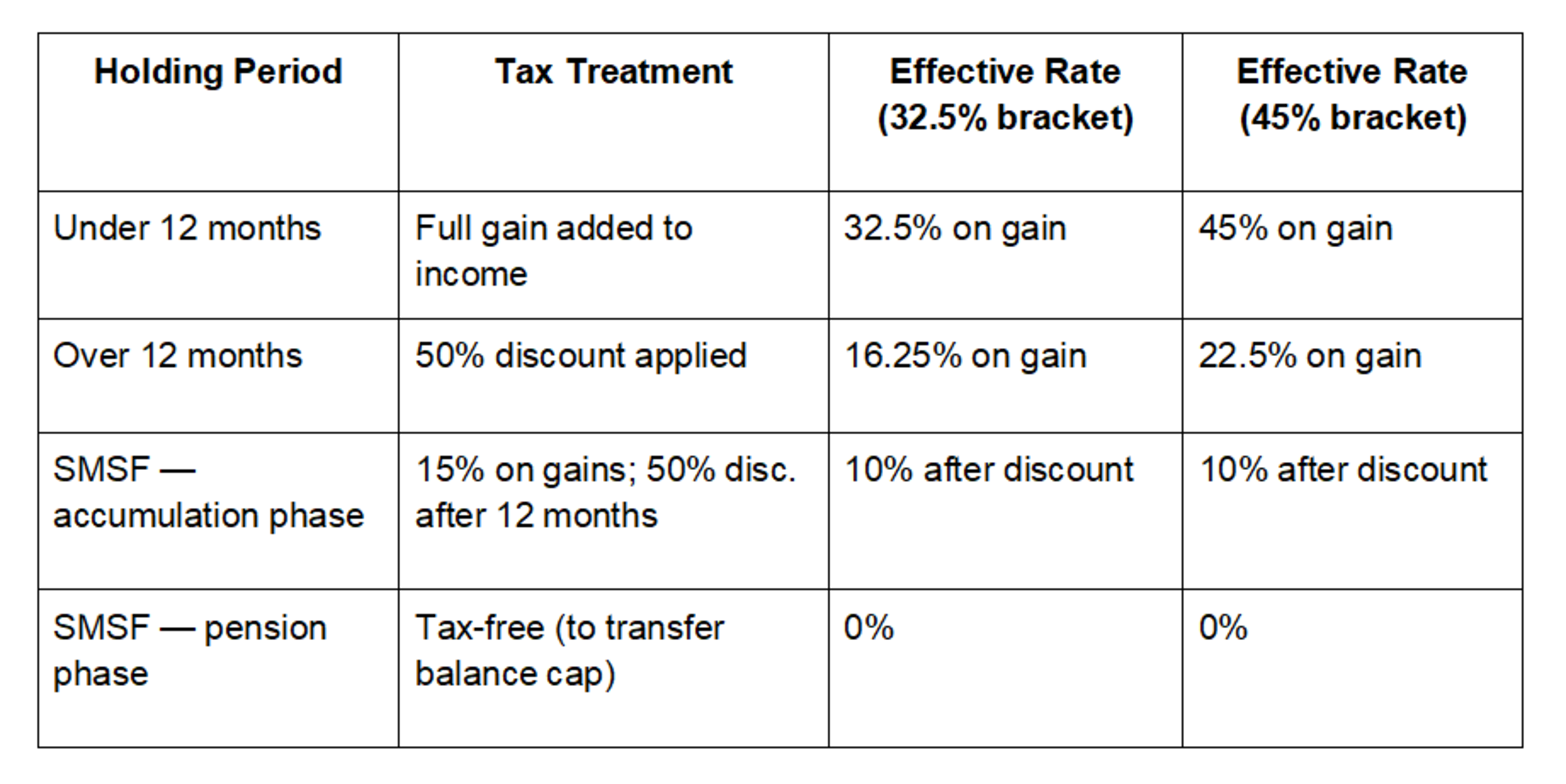

If you have held a crypto asset for more than 12 months before disposing of it, you are entitled to a 50%

CGT discount

on the net capital gain. This is one of the most powerful tax advantages available to Australian crypto investors, and the primary reason why long-term holding strategies are so compelling from a tax perspective.

Capital losses from crypto disposals can be used to offset capital gains in the same income year. Any excess losses can be carried forward indefinitely to offset future capital gains. Critically, capital losses cannot be offset against ordinary income — only against capital gains.

Wash Sale Rule:

The ATO does not permit wash sales — selling a crypto asset at a loss and quickly repurchasing the same asset primarily to manufacture a capital loss. The ATO will disregard the loss in these circumstances and may apply anti-avoidance provisions.

Where you hold multiple units of the same asset acquired at different times and prices, you must select an approved cost base allocation method. The ATO requires individual investors to use a consistent method. Traders are required to use FIFO.

FIFO (First In, First Out):

The earliest-acquired units are treated as disposed of first. This is the method the ATO defaults to for most investors.

Specific identification:

You nominate which specific units you are disposing of, based on your records. This requires meticulous record-keeping but can be used strategically to optimise which units — and therefore which cost bases and holding periods — apply to a given disposal.

As the digital asset ecosystem has matured, so too has the complexity of crypto taxation. Activities beyond simple buying and selling — including

decentralised finance (DeFi)

, non-fungible tokens (NFTs), and staking — require careful tax analysis. The ATO has issued guidance in each area, though the rules continue to evolve.

DeFi encompasses a broad range of protocols — lending, liquidity provision, yield farming, automated market makers — and each carries distinct tax implications. The central question the ATO asks is whether there has been a change in beneficial ownership.

Lending protocols:

If you deposit crypto into a lending protocol and beneficial ownership transfers to the protocol (as it typically does in most arrangements), a CGT event is triggered at the time of deposit. When you withdraw, the receipt of assets back may trigger another CGT event.

Liquidity pools:

Depositing tokens into a liquidity pool is generally treated as a disposal at current market value, triggering CGT. The receipt token (

LP token

) takes a cost base equal to the market value of the assets deposited.

Yield and interest:

Periodic income received from DeFi protocols — interest, yield, or incentive tokens — is taxed as ordinary income at the AUD value when received.

Wrapping tokens:

Converting ETH to

WETH

(or similar wrapping transactions) may trigger a CGT event if the ATO considers it a change in beneficial ownership.

Note:

The ATO's view on DeFi continues to evolve. Given the pace of protocol innovation and the complexity of beneficial ownership analysis, anyone actively participating in DeFi should maintain granular transaction records and seek specialist advice at tax time. NAX Capital's

investor education resources

can help you build a solid foundation.

The

ATO treats NFTs

as crypto assets subject to the same CGT framework as other digital assets. Several scenarios require careful consideration:

Buying an NFT with crypto:

This is a disposal of the crypto used to purchase (CGT event) and an acquisition of the NFT. The cost base of the NFT is the AUD value of the crypto at the time of purchase.

Selling an NFT:

A CGT event, with gain or loss calculated against the cost base.

Creating and selling NFTs:

If you create NFTs as part of a business, proceeds are taxed as ordinary business income. If as an individual investor or hobby creator, the treatment depends on your specific circumstances.

NFTs as personal use assets:

It is theoretically possible for an NFT to qualify as a personal use asset, but given the speculative and investment nature of most NFT activity, this exemption is unlikely to apply in practice for most collectors or traders.

Staking

and mining rewards are treated as ordinary income in the financial year they are received, valued at the AUD market price at the time of receipt. The cost base of those tokens then resets to that income figure, and any subsequent appreciation (or depreciation) when the tokens are later disposed of is subject to CGT.

If you mine crypto at a scale that constitutes carrying on a business, the ATO may treat all activity under business income rules — which removes the CGT discount but allows deduction of reasonable business expenses (hardware, electricity, etc.).

The

personal use asset exemption

is the most commonly misunderstood provision in Australian crypto tax law. Under this exemption, a crypto asset is exempt from CGT if it qualifies as a personal use asset. However, the conditions are strictly defined:

The total cost of the crypto asset must be under AU$10,000

The crypto must have been acquired and used within a short period (the ATO looks for near-simultaneous acquisition and use — typically within days)

The crypto must be used directly to purchase goods or services for personal consumption (not held as an investment first)

The crypto must not be converted to another asset (e.g., fiat, gift cards, or stablecoins) before the purchase

In practice, most crypto holdings do not qualify for this exemption. If you bought Bitcoin several months ago and later spend some of it on goods, the ATO is unlikely to accept it as a personal use asset because it was clearly held as an investment in the intervening period.

When a blockchain

hard fork

results in new tokens being distributed to holders of the original asset, the ATO's position is nuanced. Where you already held the original asset and received new tokens as a result of a chain split, the cost base of the new tokens is generally nil. However, you will realise a capital gain when you eventually dispose of those new tokens, calculated against a zero cost base. The holding period for the CGT discount begins from the date you received the new tokens, not from your original acquisition date.

For Australian investors who are serious about digital assets as a long-term allocation, the

Self-Managed Super Fund (SMSF)

structure offers tax advantages that no other vehicle can match.

NAX Capital provides

dedicated SMSF digital asset management services

tailored to meet every compliance requirement below.

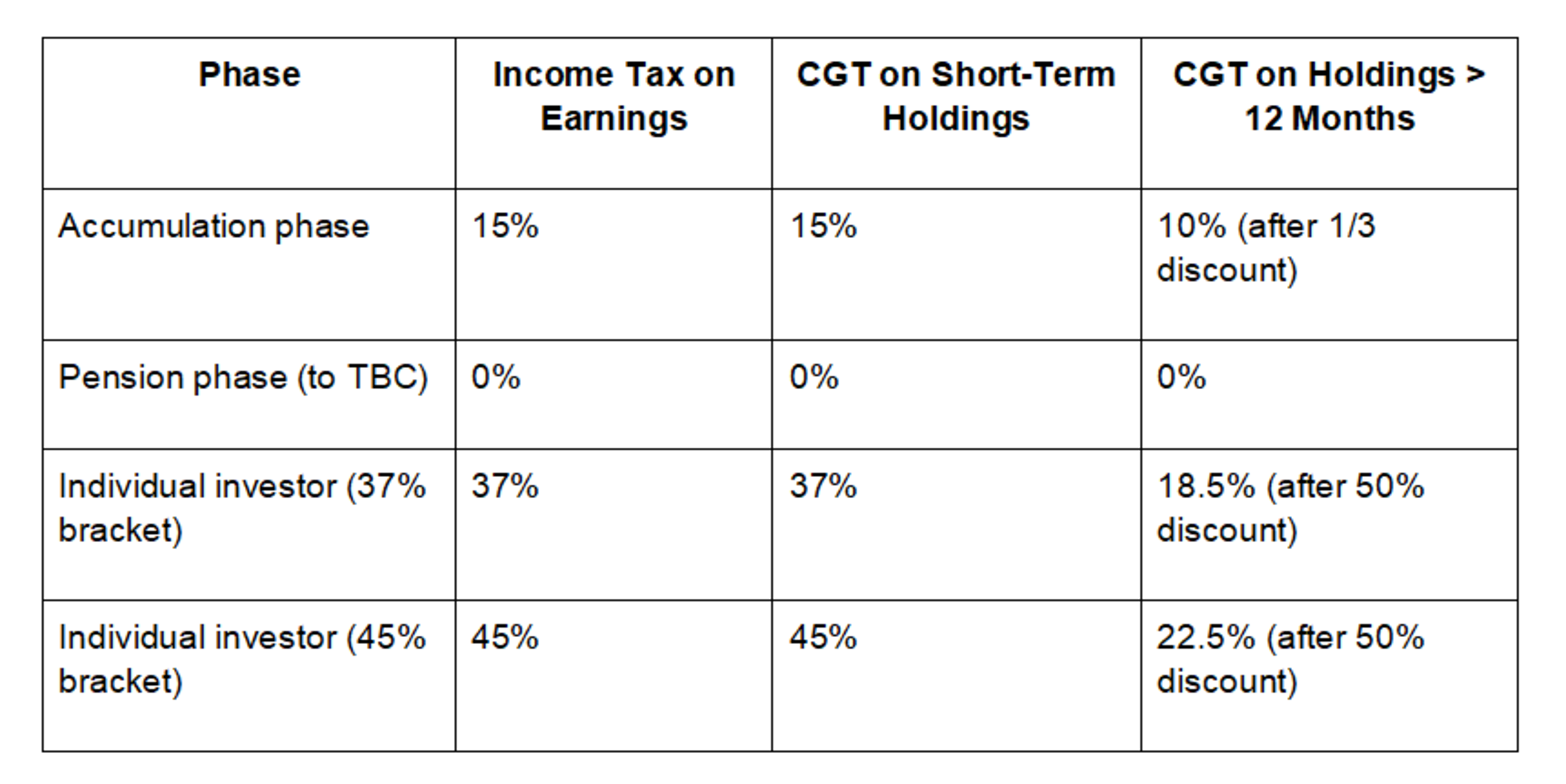

The numbers speak for themselves. A crypto investor in the 45% income tax bracket who holds Bitcoin through an SMSF in accumulation phase pays 10% on long-term capital gains. In pension phase, the same gain is tax-free.

However, SMSF crypto investing is not simply a matter of using your fund to buy Bitcoin. The

ATO

and superannuation law impose strict requirements:

Trust deed authorisation:

The SMSF's trust deed must explicitly permit the investment in digital assets. Many older trust deeds do not include this — an amendment is required.

Written investment strategy:

The fund must have a documented investment strategy that specifically addresses the rationale, risk profile, expected return, and portfolio allocation for digital asset holdings.

Sole purpose test compliance:

All investments must be made solely for the purpose of providing retirement benefits to members. The ATO scrutinises crypto holdings in SMSFs carefully for compliance with this test.

Strict asset separation:

All crypto wallets and exchange accounts must be established in the fund's name (e.g., 'XYZ Pty Ltd as Trustee for the ABC Super Fund') — not in the name of individual trustees or members. Commingling is a serious breach.

AUSTRAC

-registered platforms only:

All SMSF crypto transactions must occur through a platform registered with AUSTRAC as a Digital Currency Exchange (DCE) provider. NAX Capital holds AUSTRAC DCE Provider No. DCE 100758840-001.

No acquisition from related parties:

The SMSF cannot acquire crypto from members, trustees, or related parties — even at market value.

Annual independent audit:

The SMSF Annual Return must be independently audited each year before lodgment. The auditor will review compliance with investment strategy, asset separation, and the sole purpose test.

Pension payments in cash:

Retirement income stream (pension) payments to members cannot be made in cryptocurrency — they must be paid in AUD.

SMSF trustees who hold crypto have historically faced higher audit scrutiny from the ATO. Robust record-keeping, clear trustee minutes, and a well-documented investment strategy are essential.

Working with NAX Capital

— a brokerage that understands SMSF compliance and provides audit-ready reporting — removes significant administrative burden and risk.

Some investors assume that the decentralised, pseudonymous nature of cryptocurrency means their activity is invisible to tax authorities. This is a dangerous misconception. The ATO runs one of the most active

crypto data-matching programs

in the world.

Exchange data-matching:

Under the ATO's data-matching program, registered Australian crypto exchanges are legally required to report customer transaction data — including names, addresses, bank account details, and transaction records — to the ATO. This covers Binance, CoinSpot, Independent Reserve, BTC Markets, Kraken, and others.

International data sharing:

: Australia participates in the

OECD's Common Reporting Standard (CRS)

and has data-sharing agreements with tax authorities in dozens of countries, including those where major global exchanges are based.

Bank record analysis:

The ATO can identify fiat transfers between banks and crypto exchanges through its access to financial institution data. Large deposits to or from exchanges are flagged automatically.

Blockchain analytics:

The ATO uses commercial

blockchain analytics

tools — the same tools used by law enforcement — to trace transactions across public blockchains. Wallet addresses can be linked to identifiable individuals through exchange KYC data.

Important:

The ATO has specifically noted that it is aware many Australians have not declared crypto income or gains. The agency has said it will contact taxpayers who it believes have not met their obligations. Voluntary disclosure before the ATO contacts you typically results in significantly reduced penalties.

Assuming crypto-to-crypto swaps are not taxable (they are — every swap is a CGT event)

Failing to record the AUD value at the time of each transaction (not just when you sold)

Not declaring staking rewards and airdrops as income

Attempting wash sales (the ATO will disallow the loss and may apply penalties)

Confusing SMSF and personal assets (all crypto owned by the fund must be held separately from personal holdings)

Losing records when an exchange collapses (export your full transaction history from every exchange regularly — do not rely on the platform to maintain them)

The ATO requires all crypto investors to maintain records for a minimum of five years from the date of each transaction — or five years from when you lodge the tax return in which the transaction is declared, if later. For assets with long holding periods, this can mean records spanning a decade or more.

For each transaction, your records should capture:

The date of the transaction

The type of transaction (purchase, sale, swap, staking receipt, airdrop, gift, etc.)

The amount of crypto involved (in the native unit, e.g. 0.5 BTC)

The AUD value at the time of the transaction (use the spot price from a reputable source or your exchange's price at the time of the trade)

The exchange or wallet involved

Any fees paid (in AUD or crypto)

Proof of ownership of wallets (relevant for inter-wallet transfers)

Practical Tip:

Export your full transaction history from every exchange you use at the end of each financial year (30 June). Do not assume the exchange will retain this data indefinitely — several major exchanges have closed or restricted account access without notice. Purpose-built crypto tax software such as

Koinly, CryptoTaxCalculator

or

CoinTracking

can import exchange data via API, convert transactions to AUD automatically, and generate ATO-ready tax reports.

Tax minimisation — arranging your affairs within the law to reduce what you owe — is entirely legitimate. Here are the strategies most commonly available to Australian crypto investors:

The single most powerful tax reduction strategy available to Australian crypto investors is simply holding. By holding an asset for more than 12 months before disposing of it, you halve the effective CGT rate. For investors in the 45% income tax bracket, this reduces the effective CGT rate from 45% to 22.5%. Patient investors are structurally advantaged by Australian tax law.

If you hold crypto assets that are currently sitting at unrealised losses, selling them before 30 June allows you to crystallise those losses and offset them against capital gains elsewhere in your portfolio. This strategy —

tax-loss harvesting

— can significantly reduce your net CGT liability for the year. Remember: you cannot manufacture artificial losses through wash sales, but genuine strategic disposals of loss-making positions are entirely legitimate.

If you are considering selling an asset that will generate a large capital gain, consider whether delaying the sale to the next financial year (after 1 July) might be advantageous — for example, if you anticipate lower income (and therefore a lower marginal rate) in the following year. Similarly, if you are approaching the 12-month mark for a significant holding, waiting until that threshold is crossed before selling halves your CGT liability.

For long-term investors with significant capital, the SMSF structure offers the most favourable tax treatment for digital asset gains available in Australia. As detailed above, long-term CGT rates within an SMSF accumulation account are 10%, falling to zero in pension phase. The establishment and ongoing compliance costs of an SMSF are meaningful, but for investors with portfolios of sufficient scale, the tax savings are substantial.

Speak to the NAX Capital team

to explore how an SMSF strategy could work for you.

Depending on the nature of your crypto activity, various expenses may be deductible. These can include brokerage and advisory fees directly related to managing your portfolio, costs associated with a mining operation carried on as a business, and accounting fees for crypto tax preparation. Including

NAX Capital's OTC brokerage fees

as part of your cost base is one practical example of a legitimate, claimable cost. Consult a qualified tax adviser to determine what applies to your circumstances.

Tax planning for crypto is not a year-end exercise — it is a 12-month discipline.

Investors who review their portfolio positions, holding periods, and unrealised gains and losses on a quarterly basis are consistently better positioned than those who scramble in June to understand their exposure.

The regulatory and tax environment for digital assets in Australia is evolving rapidly. Several developments are directly relevant to investors in the 2025–26 financial year and beyond:

ATO tax bracket changes:

The

ATO announced income tax cuts

and changes to tax brackets for the 2026 financial year. These changes affect the marginal rates at which crypto gains are taxed for individuals — review the updated brackets with your tax adviser when calculating your position.

Digital asset licensing framework:

The

Australian Treasury

is developing a comprehensive licensing framework for digital asset platforms, expected to come into effect in 2026. The framework will bring more crypto businesses under

ASIC

oversight and create clearer obligations for service providers. Robust record-keeping now will make any future compliance review straightforward.

ATO data-matching expansion:

The ATO continues to expand the scope of its data-matching program, with increasing coverage of decentralised exchange activity and cross-border transfers. Investors should assume that the ATO has access to data from any platform with identifiable Australian customers.

May 2025 court ruling on Bitcoin:

A court ruling in May 2025 may have future implications for the classification of Bitcoin and potentially other major digital assets. Specialist commentary from crypto tax advisers is ongoing — watch for ATO guidance updates following this decision.

SMSF audit attention:

The ATO has indicated continued focus on SMSF compliance in the digital asset space, particularly around asset separation, trust deed adequacy, and investment strategy documentation. Trustees should review their compliance documentation proactively.

Cryptocurrency taxation in Australia is complex, but it is not unknowable. The

ATO

has published substantial guidance across CGT, income tax, DeFi, NFTs, and SMSF investment — and the core principles, once understood, are consistently applicable.

The investors who navigate Australian crypto tax most successfully share three characteristics: they maintain meticulous records from day one; they structure their investments with the 12-month CGT discount in mind; and they work with professionals — accountants, tax advisers, and

licensed brokers like NAX Capital

— who understand both the technical and the fiscal dimensions of digital asset investing.

Compliance is not a burden to be minimised. It is the infrastructure that protects the value you have worked to create. In a market where the ATO is increasingly sophisticated, and where Australia's digital asset regulatory environment is converging toward institutional standards, the investors who treat their crypto portfolios with the same professional rigour they bring to shares or property will be the ones who come out ahead.

Ready to invest with confidence?

NAX Capital

provides institutional-grade

brokerage, custody

, and

OTC execution

for Australian investors — with the compliance infrastructure and reporting standards that serious capital demands. Contact our team to discuss how we can support your digital asset strategy.

This article is published for general informational and educational purposes only. It does not constitute financial, tax, or legal advice. Tax laws are subject to change, and the information in this article reflects the ATO's published guidance as of the 2025–26 financial year. Individual circumstances vary significantly — always consult a registered tax agent, qualified accountant, or financial adviser before making decisions about your crypto tax position. NAX Capital is the commercial name of Peer TC Pty Ltd (ACN: 651 368 213),

AUSTRAC

DCE Provider No. DCE 100758840-001.